Introduction:

Some patterns and events recur regularly in our environment, influencing our behaviour and our lives. This can be seen in various instances throughout our planning schedules and routines – from planning our holidays based on the seasonal cycle to planning our work, recreation and sleep based on the regular day cycle.

We depend on this knowledge of recurring patterns so we won’t have to reconsider every decision from scratch.

Economies, companies and markets also operate pursuant to such patterns, which are commonly known as cycles. Not only do they arise from naturally occurring phenomena, they also come from the ups and downs of human psychology and from its resultant human behaviour. Since human psychology and behaviour play such a big part in creating them, these cycles aren’t as regular as the cycles of clock and calendar, but they still give rise to better and worse times for certain actions. And they can profoundly affect investors.

A cycle can last anywhere from a few weeks to a number of years, depending on the market in question and the time horizon at which you are looking. A day trader using five-minute bars may see four or more complete cycles per day while, for a real estate investor, a cycle may last 18 to 20 years. Although not always obvious, cycles exist in all markets.

If we pay attention to these cycles, we can come out ahead. If we study the past cycles, understand their origins and import, and keep alert for the next one, we don’t have to reinvent the wheel in order to understand every investment environment anew.

Market Cycles:

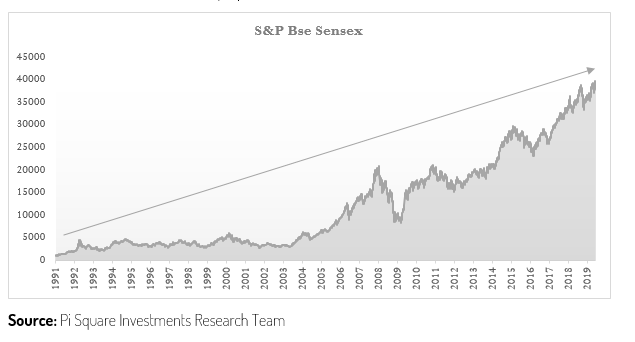

Equities are often called compounding machines and rightly so. In the long run equities as an asset class has proven to outperform all other asset classes.

However, except in a perfect world, the run to the top is not a straight line, even though in the long term it might look like that. The journey to the top is often interceded with intermittent ups and downs.

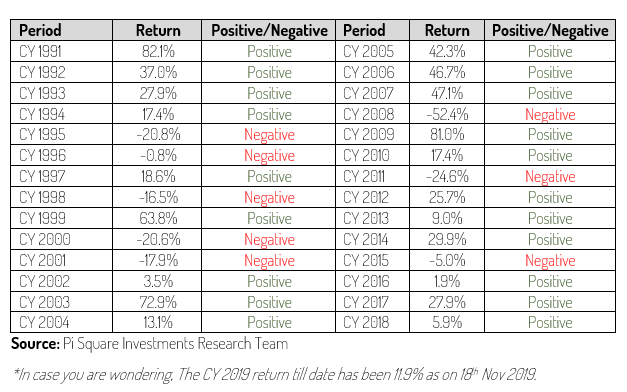

If we take a look at Sensex for example:

This chart displays the Pi Square Investments ‘Journey Through the Cycles’ framework. It maps market environments across an X-axis representing time and a Y-axis representing different cycles. It details various market phases, highlighting the path of market expansion, structural shifts, peak performance indicators, and structural troughs. The graphic serves to visualize how investment portfolios navigate changing economic cycles over prolonged periods.

Out of the past 28 years, in only 8 years has the index shown a negative performance which means there would be a 28.6% probability of a poor return.

Rather than aberrations these ups and downs are ‘cycles’ that are integral to the markets and a combination of many such cycles is what the market represents.

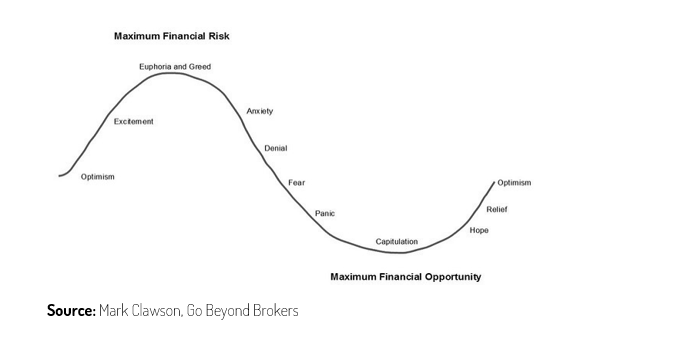

A typical cycle looks like the figure below.

These cycles are a series of events which not only follow each other but each phase also causes the next. Even though it is impossible to gauge the time or magnitude of each phase, the events of each phase invariably lead to the next phase and the events of that phase lead to the next and so on. So even though in the long term the equity market is expected to trend upwards, such phases are important when taking investment decisions since they indicate important clues about the direction of the market and ultimately will have a bearing on the return.

A cycle typically moves around a mid-point, or as it is more formally called the phases always ‘regresses or reverts to mean.

The cycles of expansions are characterised by business optimism and expanding business profitability. Conversely, cycles of contraction are characterised by business pessimism and declining or stagnating business profitability. Markets anticipate these fluctuations and move ahead.

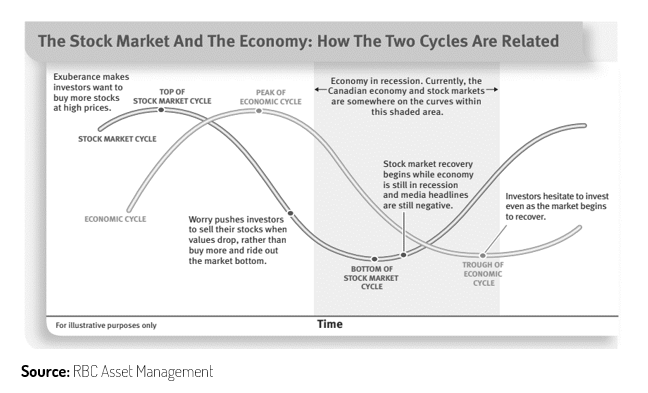

Markets start moving up ahead of a boom phase and continue to expand during the boom phase finally declining sharply or crashing anticipating a sharp slowdown or recession.

Similarly, markets anticipate a recovery and boom and start moving up much ahead of actual economic recovery. From investors’ perspective, the turning points in the business cycles are hugely important. Investors who can anticipate the cyclical swings ahead of the market can make a fortune.

“The Three Stages of a Bull Market”: the first stage, when only a few unusually perceptive people believe things will get better, the second stage, when most investors realize that improvement is actually taking place, and the third stage, when everyone concludes things will get better forever.” – Howard Marks

Industry/Sector Cycles:

Not only such cycles are evident for the country as whole but also in specific industries.

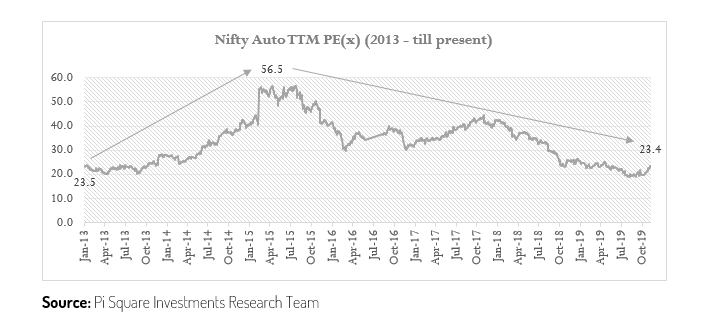

Automotive Sector

The Automotive industry in India is a case in point. In 2013, auto companies were trading at low P/E. A low P/E often means that the industry’s future is not bright and that an earnings decline is expected. A purchase of automotive industry stocks then however would have been in line with Buffett’s mantra: “Be greedy when others are fearful”. Over the next 5 years, these stocks were very profitable where in the Auto Index grew at a 20% CAGR compared to the Nifty index which grew only at 12% CAGR.

Post 2018, a major fall in automobile sales was seen due to several factors which include the low affordability (high interest & insurance costs) and an uncertainty about the changes in the engine regulations (Bharat VII and Electric Vehicles Policy).

This led to a drastic fall in the automobile stock prices.

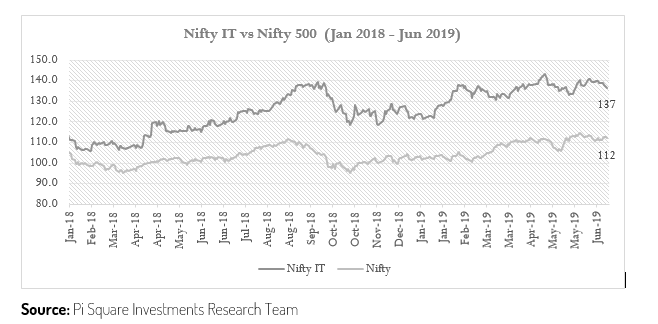

IT Sector Rally between January 2018 to June 2019

Between January 2018 and June 2019, the IT sector had seen a major upwards cycle (bull run) and had drastically outperformed the index.

This was due to the rise in income for the IT companies, whose revenue is primarily earned in US $ terms, due to the depreciation of the Indian Rupee along with other currencies of the emerging markets vs the US Dollar.

“Stock market goes up or down, and you can’t adjust your portfolio based on the whims of the market, so you have to have a strategy in a position and stay true to that strategy and not pay attention to noise that could surround any particular investment.” – John Paulson

Stock Cycles:

Companies also follow similar economic cycles just like market cycles and industrial cycles. Many such instances can be seen throughout like Sun Pharma and Hindustan Unilever

Such stock cycles can be impacted by valuation mismatches, valuation disparities, growth outlooks and other macroeconomic factors

Sun Pharma

In April 2014, Sun Pharmaceutical acquired 100% of Ranbaxy Laboratories for $4 billion to create world’s fifth largest specialty generic pharma company

“In business, financial and market cycles, most excesses on the upside — and the inevitable reactions to the downside, which also tend to overshoot — are the result of exaggerated swings of the pendulum of psychology. Thus, understanding and being alert to excessive swings is an entry-level requirement for avoiding harm from cyclical extremes, and hopefully for profiting from them.” – Howard Marks

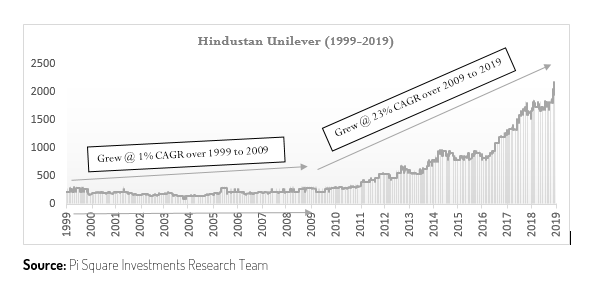

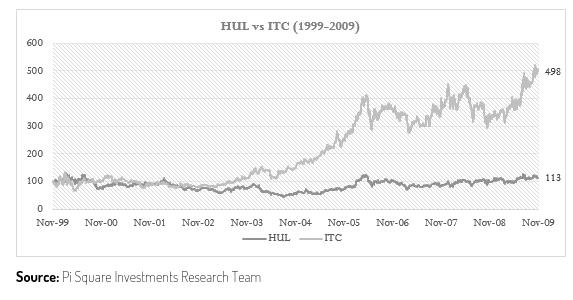

Hindustan Unilever

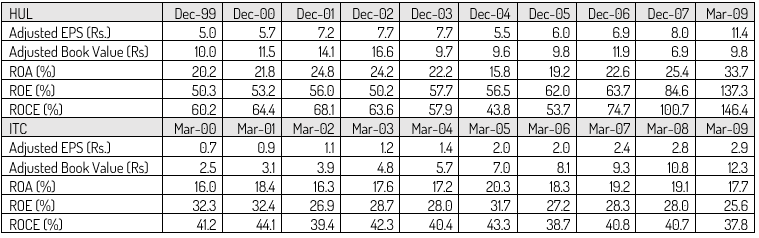

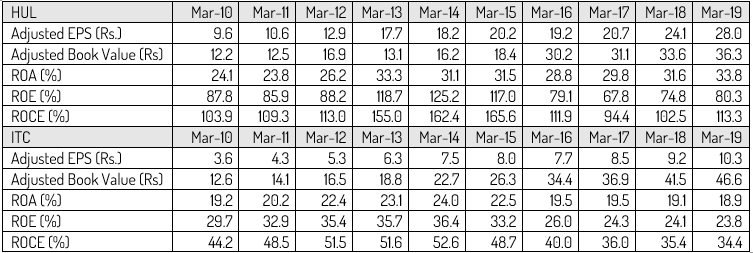

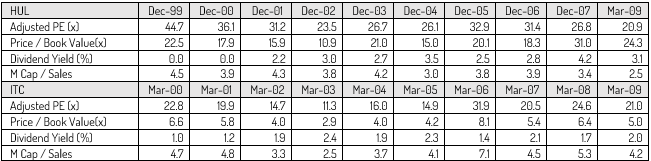

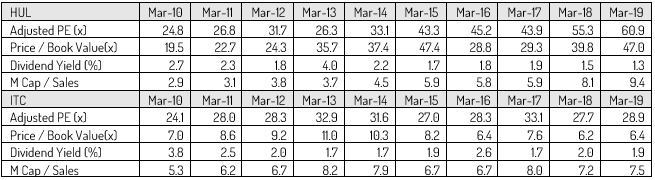

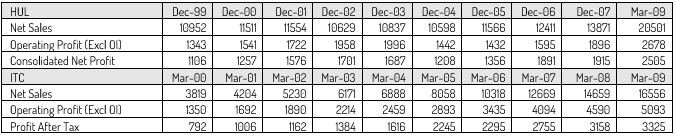

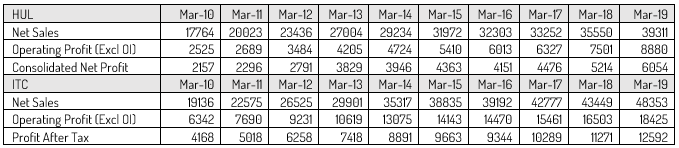

One of the now considered most favourite stocks, Hindustan Unilever (HUL) has seen a mixed journey over the past 20 years.

Between 1999 and 2009, HUL investors did not reap any handsome returns as it merely grew by a 1% CAGR during that period. On the other hand, ITC – another major FMCG brand, grew by 5 times.

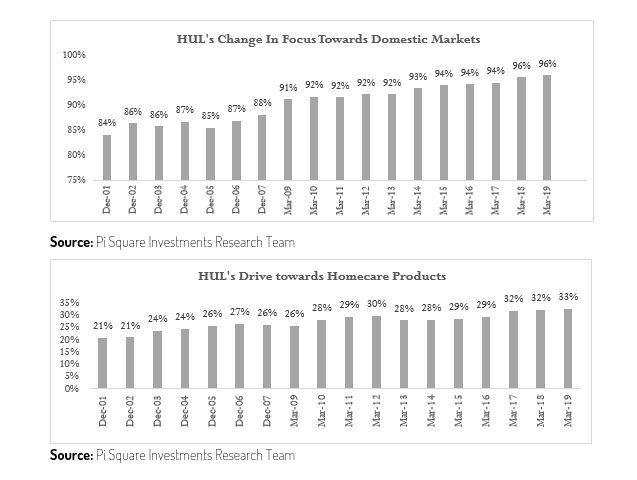

At the turn of the decade, between 2009 till 2019, HUL’s stock considerably outshined its fellow peer ITC’s performance. This was on the back of strong growth numbers, improvement in margins and most importantly HUL’s exponential growth in its domestic distribution network.

Conclusion:

Market movements can often be too tough to handle, especially when it mirrors an investor’s mood swings! As investors, we tend to make changes in our portfolio by pitching into to stocks that we believe will work. The next month or so is going to be specifically volatile for the Indian markets and with our country set on the outset of an election, one thing is certain — the market will be unpredictable.

| SEBI Registration Details | |

| Registered Name | Pi Square Advisors |

| Type of Registration | Non-Individual Investment Advisor |

| Registration No. | INA000018179 |

| Validity | July 05, 2023 – Perpetual |

| BASL Member ID | 2018 |

| Grievance Redressal / Escalation Matrix | |

| CEO/Principal Officer : Vishrut Pathak | |

| Email: principalofficerpisquare@gmail.com | Phone. No.: +91 2717 459 271 |

| Grievance/Compliance Officer : Bhoomi Godhani | |

| Email: compliance@pisquareinvestments.com | Phone. No.: +91 2717 459 271 |

| Address: B 1808, Navratna Corporate Park, Ambli Bopal Road, Ahmedabad – 380058 | |

| Working Hours: Mon-Fri: 10am to 6pm (except public holidays) | |

In case of any grievances or complaints, please write to us on complaints@pisquareinvestments.com Additionally, you may also reach SEBI SCORES and download the SEBI SCORES app from Play Store and App Store.

© 2018 Pi Square Investments – All Rights Reserved